An Introduction to the World of Airline Economics

COVID-19, Occupancy, and Oligopolies

The Department of Transportation has made a rare publication exception during the COVID-19 pandemic, and you can now access a wide array of data regarding flight schedules and operations for all flights operating in the United States.

As I know that a majority of you have vested interests and comparative advantages elsewhere, I’ve taken the liberty to clean up these data sets and put them into something readable. I’ve quickly learned that the wonderful world of aviation is painstakingly complex, largely thanks to regulatory and bureaucratic constraints, so I hope that this first series of airline-based economics posts can simplify what I’ve found to be the largest areas of importance. As we approach the one-year mark of lockdowns and quarantines, what better place to start than with the first shocks to the industry?

If you want to see my initial predictions on what impact the pandemic would have on the aviation industry, you can find my Hill article here.

First, let’s talk about terminology.

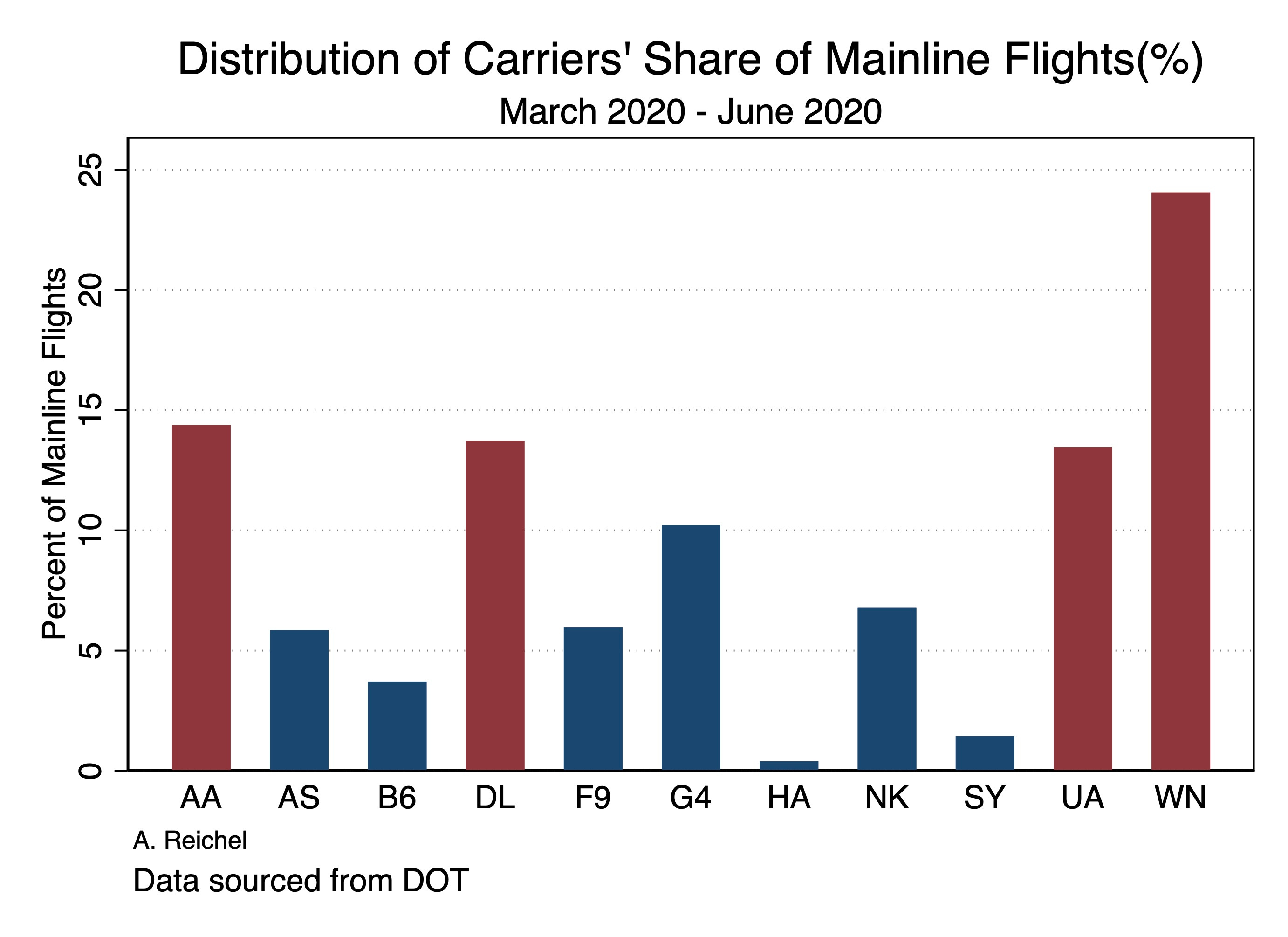

The term “mainline carriers” typically applies to large-scale passenger airliners that commonly operate via hub-and-spoke networks, whereas the term “top four” often refers to the top four major mainline carriers in the United States; Delta (DL), American Airlines (AA), United (UA), and Southwest (WN). Mainline carriers often own or operate with “regional carriers” based on alliances or codesharing. Regional carriers generally operate much smaller aircraft, seating up to 75 passengers on average, while mainline carriers average well over 100 passengers per flight.

“Low cost carriers”, commonly referred to as LCCs, embody carriers that emphasize minimizing operating costs on the margins of reducing traditional services and amenities, with chief examples being Spirit and Frontier.

Lastly, “occupancy” is the number of enplanements (actual number of passengers flown per flight) divided by the passenger capacity of the aircraft being flown, and typically is representative of demand for individual flight routes.

Demand Shocks and Occupancy Dips

Now, let’s rewind back to March-June of 2020, often seen as the period encompassing the most-strict lockdowns in the United States as a whole.

The most obvious effect of the COVID-19 pandemic on air transportation has been a stark decline in demand for travel. As the world shut down, aviation was amongst the first industries rattled by lockdowns. Focusing specifically on mainline carriers, occupancy as a whole experienced an overwhelming crash, with market power remaining in favor of the top four.

The battle for market power has been ever-present in the airline industry, but became an even larger topic after the mergers of 2007-2014 left four airlines with 80% of the market share. Just before the pandemic, American Airlines topped the board in terms of passengers with Delta as a close second, and Southwest and United ranking third and fourth respectively with nearly 20% less passenger volume.

Southwest was able to gain substantial ground in terms of market share over the past year, while American, Delta, and United each individually held just under 15% of the market. Southwest unsurprisingly levied power from strong domestic routes and lower marginal costs, with their lack of first cabin allowing them to substantially lower fares for all seats and experienced a similar affect post-911, eventually rising from an LCC to mainline carrier in the mid 2000s. The true survivors of the pandemic will be those who can levy low marginal costs and successfully reduce price with the least harm.

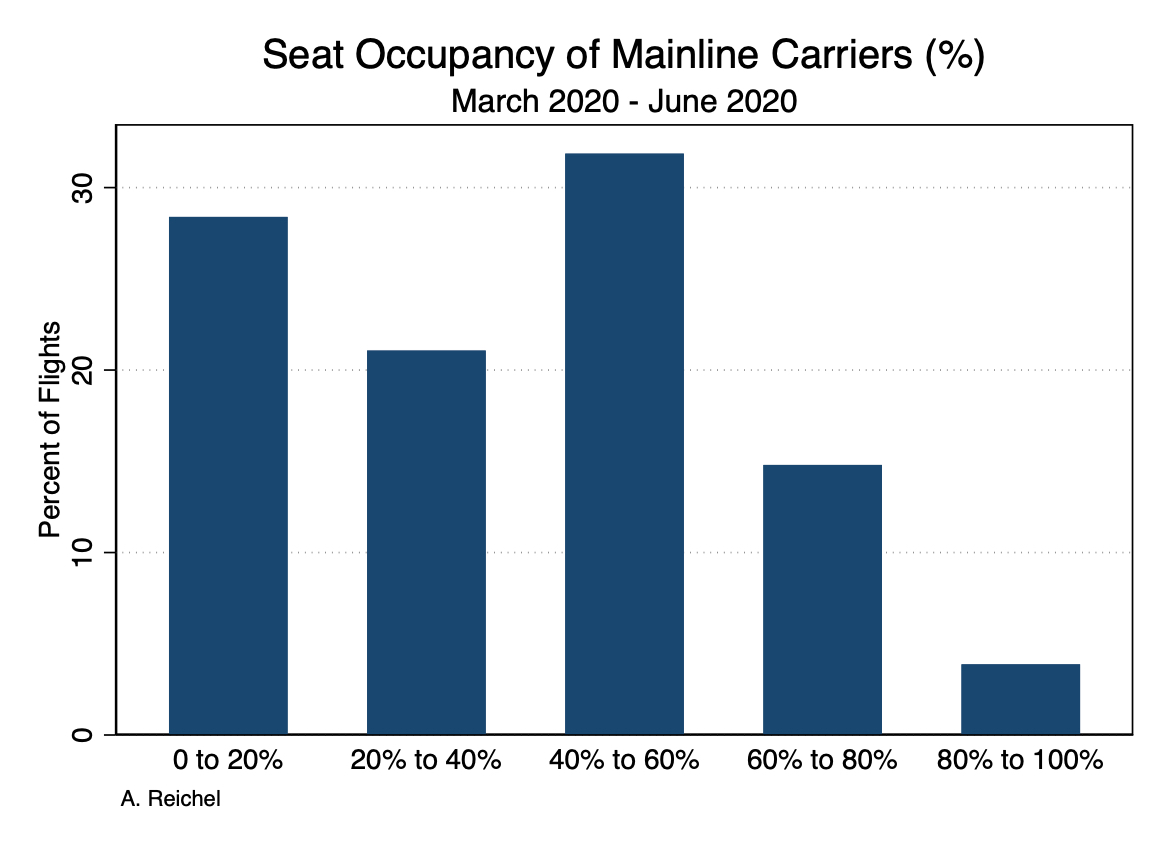

The distribution of occupancy was startling- with over 80% of flights operated by mainline carriers falling short of 60% occupancy.

A good majority of the early fall in occupancy can be attributed to enhanced safety measures that prevented aircraft from flying at full capacity, but was sustained by a fall in demand that has lasted to the present day. TSA traveler throughput provides a fantastic estimate of overall passenger traffic, and in the last two weeks of April fell to an approximately daily level of 97,000 passengers compared to the 2.5 million daily throughput on the same days in 2019. The latest figures are summarized in the table below.

Vertical Integration and the Advantages of Delta and Southwest

As I lightly mentioned in the Hill article, and predicted back in March of 2020, Delta and Southwest have fared much better than their mainline competitors, American and United. This is largely thanks to strong domestic networks held by both Delta and Southwest, whereas American and United fail to capture demand on domestic routes, Delta and Southwest have been successful in picking up. Why? Codesharing.

Code sharing is the process by which major airline carriers can contract smaller regionals to transport passengers onto the major’s network. American and United rely heavily on codesharing domestically, where Delta tends to fly domestic routes and codeshare for international flights through alliances. Often, major airline carriers subcontract regional carriers on shorter routes in order to transport individual passengers from smaller subsidiary airports to the airline carriers’ hubs. Subcontracting occurs as regional airliners have a great cost advantage in operating smaller aircraft and thus frequenting shorter routes.

Regional airlines typically operate via codeshare agreements with major carriers. Codeshare agreements are business arrangements by which two or more airlines publish and market the same flight under the IATA airline flight code and designator number of the larger airline (via the IATA Standard Schedules Manual). Flights are typically operated by one major airline also known as the “administrating carrier” or “marketing carrier” while sears are sold by the cooperating smaller partner.

In simple economic terms, carriers will make the decision to contract out when the cost of flying an additional route is too costly for them. Major carriers tend to have larger aircraft, meaning more seats to fill and higher operating costs, and the complexity of airport scheduling can be simplified if carriers can make agreements with each other on regional routes. However, as the pandemic placed external constraints on international travel due to travel bans, carriers with strong domestic networks have had a great advantage. The marginal cost of contracting out now exceeds the marginal cost of flying routes that were previously too costly as carriers fight to establish dominance on stable domestic routes. In addition, airliners with slots at key airports went so far as to fly empty planes in order to keep them.

While Delta Airlines ranks below American Airlines in terms of enplaned market share, it is ranked as the best in class operator in the United States. Delta is part of a global network and leverages domestic power mainly through its Hub in Atlanta, Georgia where it holds approximately 73% of the market share- more than any network carrier at any hub airport. In addition to Atlanta, Delta has eight other domestic hubs and four international hubs in France, Amsterdam, England, and Japan. Southwest follows a similar model, creating networks through eleven operating bases across the country with a fleet size of 752 aircraft. Both Delta and Southwest can leverage their network effects by connecting travelers via hubs and operating bases, reducing both the cost and time of travel for their customers, and rely less on the complexities posed by code-sharing regional travel. Delta and Southwest also boost higher ratings than competitors, and experience much larger profitability- in 2018 Delta and Southwest ranked as the top two carriers in terms of net profits at $3.9 billion and $2.5 billion respectively. In terms of the future, Delta is currently in the process of expanding network routes which will only facilitate its growing market power, and in 2019, Southwest launched new routes to Hawaii, which exceeded company expectations and boosted earnings.

Another crucial aspect of Southwest’s success is their dedication to efficiency. As United and American struggled to develop new methods of boarding that complied with enhanced sanitation and social distancing measures, Southwest had implemented back-to-front boarding at a number of airports across the nation.

Thinking Rationally

What is the economic efficiency of an oligopoly? Or is there one? The praxis of rationalization in economics says that there must be- firms wouldn’t behave in this way if it was not beneficial to them in some other way. However, if this oligopoly structure is not supplementary in hedging risks against major exogenous shocks, then perhaps a greater investigation needs to be done as to why we see the emergence of such orders.

And speaking of oligopolies, one final thing to think about- the main four typically champion for regulatory means such as slot allocation, in the name of reducing congestion. Interestingly, even during the pandemic and a period of low passenger traffic, congestion at slot controlled airports is significantly higher than the average congestion across all airports, with a majority of the distribution of delays being both carrier-caused and over three hours. If slot allocation can’t even serve its main goal, might there be other supply-side implications- perhaps those that allow airlines to lobby for barriers to entry- involved in keeping power concentrated amongst themselves?

But more on that later.

TIL WN means southwest

also did it hurt when you fell from heaven like a piece of engine debris?

Congrats on becoming an author