It's Deeper Than $6 Trillion

Happy Wednesday everyone!

I apologize for the delay in uploading; I was traveling for quite a bit of April and finishing up final exams and papers, as well as changing jobs, and decided to take a break from the Substack to ensure quality of work.

A Look at Biden’s Budget

On May 27th, 2021, it was announced that President Joe Biden planned a $6 trillion budget proposal for the 2022 fiscal year. This proposal pushes fiscal spending as a proportion of GDP to its highest level since World War II, and over the next decade, deficits would be expected to run somewhere north of $1.3 trillion.

President Biden formally proposed the budget on Friday, May 28th, 2021, but even prior, documents obtained by the New York Times have sent markets and investors (and people on the internet) into a frenzy.

What do we know about the budget proposal?

According to the New York Times, Biden’s proposal anticipates that the federal government will spend $6 trillion for the 2022 fiscal year, which will rise to a whopping $8.2 trillion by the year 2031. Deficits for 2022 are anticipated to total around $1.8 trillion and span over the next decade at around $1.3 trillion yearly.

If you recall previous fiscal packages, such as the American Rescue Plan and the American Jobs Plan, President Biden has been focused on bolstering growth for low-income and middle class Americans, restoring jobs, building a “new economy,” and even reducing pollution and fostering a greener future.

Infrastructure has been a huge theme — which is a relatively good thing. The federal spending that has been happening isn’t going to inert government projects, but is instead being used to create lasting jobs and put the United States in a better position to outcompete China. Simply put, the dollars spent will go towards an attempt to spur productivity and growth, and give America a leading edge on a global scale.

Per the New York Times, proposed projects include roads, water pipes, broadband internet, electric vehicle charging stations, and manufacturing research, in addition to an abundance of other growth initiatives that will be unveiled once the proposal is released.

President Biden isn’t alone in his ambitious plan to get people back to work and create new jobs— Federal Reserve Chairman Jerome Powell has stressed a similar sentiment on the importance of job recovery over inflation concerns, and the Fed has kept monetary policy loose in order to accomplish this goal.

But there’s another important question — will spending exceed $6 trillion? It’s possible. What Biden’s budget plan doesn’t include is funding for a public health care option, something that the President has made a key part of his platform and continues to voice support for. Instead, Biden will look to congress for the potential implementation of a public health care option, which will surely add more pork to the pie and bolster budget numbers.

So what does this mean for the economy?

The fiscal packages we’ve seen over the past six months (and the proposed budget) fall under the category of discretionary spending, with most financed by deficit spending. In terms of economics and the American political system, discretionary spending refers to appropriations under the control of congress that are subject to budget rules and constraints, such as defense and education, that are separate from mandatory spending and entitlement programs, as defined by the Congressional Budget Office.

While discretionary spending refers to the nature of appropriations (differentiated from mandatory spending), deficit spending refers to the nature of how the spending is financed.

I’ve mentioned this in other articles, but wanted to recap on the two main ways to fund large government projects; through revenues or via deficit spending, with the excerpt below.

Deficit spending is any spending that exceeds revenues and the budget deficit, and is financed through borrowing as opposed to via taxation … There are a few ways in which governments can finance deficit spending, with one of these ways being through the sale of government securities and Treasury bonds. In addition, the funds can be minted through an expansion of the money supply.

Is the Economy Overheating?

Initially, deficit spending will front the costs of the budget, however, the President has plans to significantly raise taxes on corporations and the wealthy that will span well into the future.

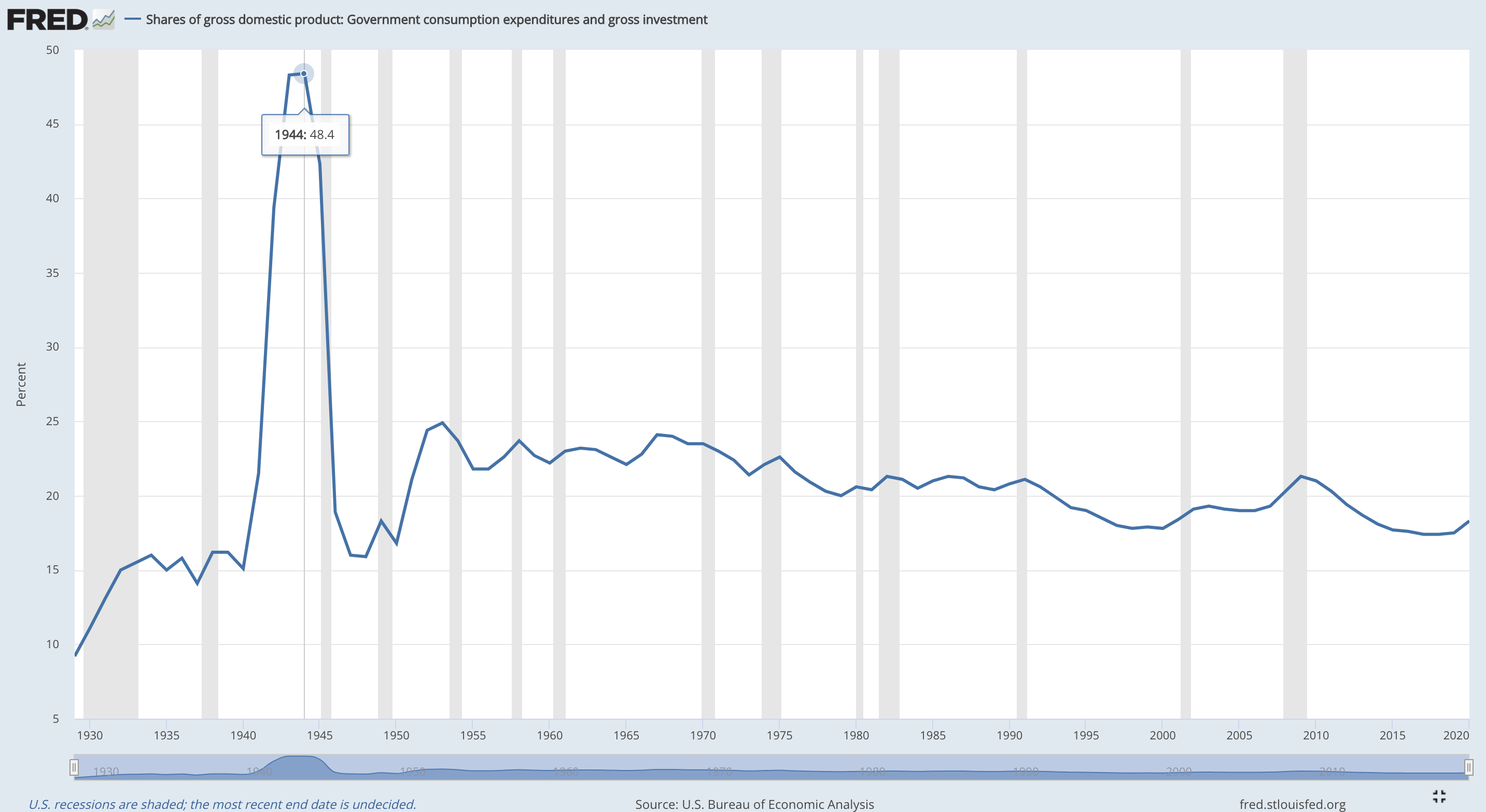

If the budget is passed and implemented, fiscal spending as a share of GDP will hit its highest percent since WWII.

Shares of gross domestic product: government consumption expenditures and gross investment. Highlighted is government spending as a share of GDP in 1944, at its all time high of 48.4%. Graph sourced from FRED.

The most common rebuttal I’ve seen is something along the lines of “But the late 40s-50s was a post-war period!” While it’s very true that a post-war economy greatly differs from the economy we live in today, that shouldn’t negate the fact that we have experienced one of the largest exogenous shocks in economic history. The COVID-19 pandemic and subsequent lock-downs embody similar underlying themes for labor and production that will require some level of spending to return to pre-COVID levels of employment and productivity.

In addition, as the NYT also remarked on, Biden’s team of economists are currently undershooting growth. When growth is undershot, economies can run the risk of overheating.

While growth in the form of GDP is expected to hit highs that we haven’t seen in 40 years by most economists outside of the White House, the recent jobs report was much lower than anticipated, initially curtailing hawkish sentiment. Reasons for low job growth stem anywhere from continued business closures to favorable unemployment compensation and wage rigidities.

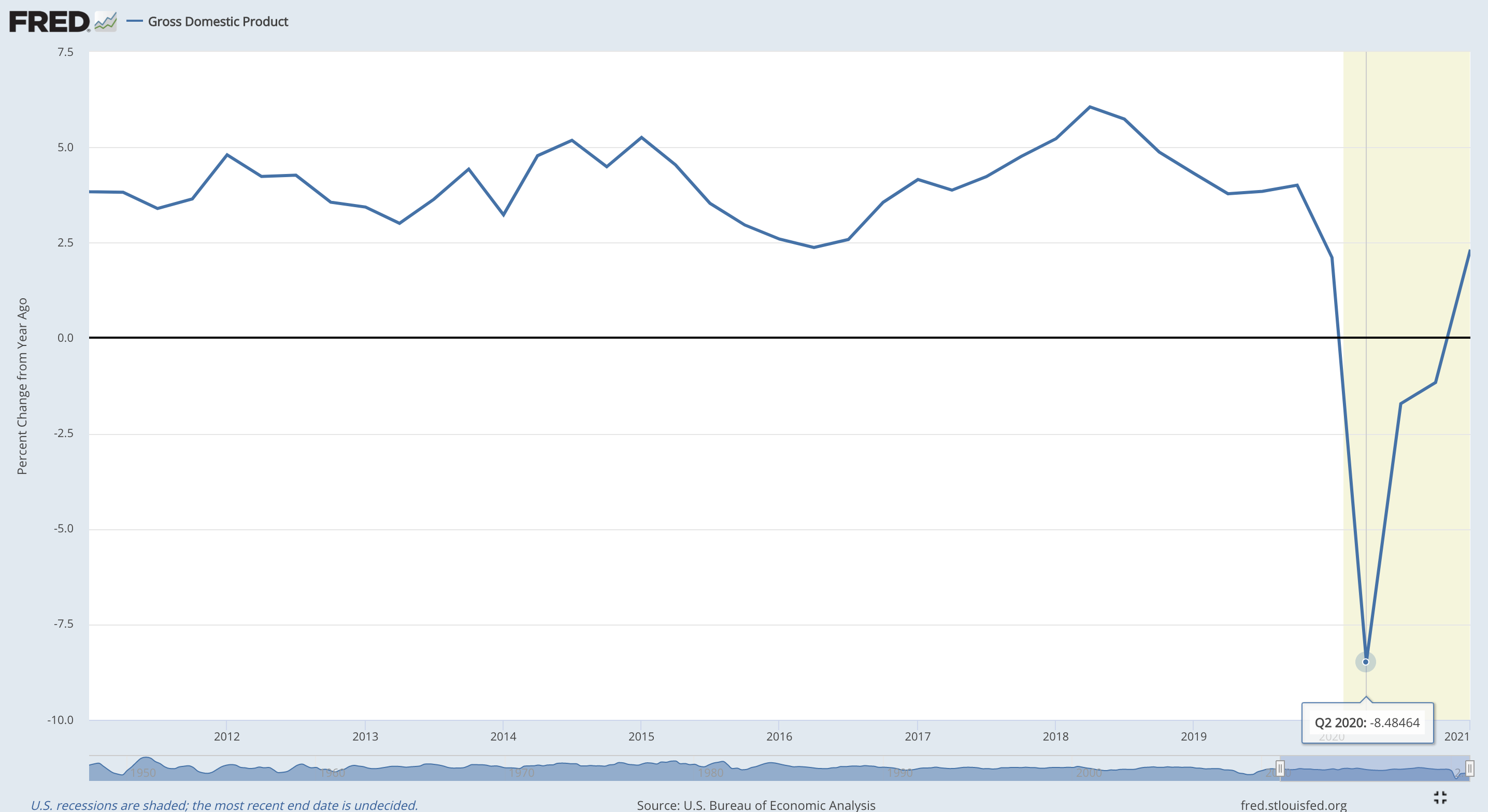

Gross Domestic Product, Percent Change from One Year Ago, Quarterly, Seasonally Adjusted. Highlighted is the Q2 2020 GDP % change from one year ago at its pandemic low of -8.485%. Graph sourced from FRED.

GDP has exhibited a V-shaped recovery since its Q2 percent change low of -8.485%, and so long as the vaccination rollout and COVID-19 pandemic aren’t faced with any additional challenges, there is no reason to expect that “the return to normal” will be delayed any further than early next year.

The risk we run with undershooting growth expectations and being generous with fiscal spending is that of exceeding our productive abilities (PPF) and eventually needing to correct the excess unsustainable growth, which could result in upward pressure on inflation. Speaking of inflation . . .

Is inflation on the horizon?

Hold your money printer memes! As I mentioned above, this budget proposal is set to be financed with deficit spending and an increase in tax rates — but that doesn’t mean we should rule out a rise in inflation, just that it won’t come from “money printing.”

I’m standing true to my estimate of the U.S. exceeding no more than 6% inflation this summer (as in 6% core inflation, not the change in CPI), and no impeding hyper-inflation this year, so long as the Fed sticks true to its promise of responding quickly with its toolkit (a.k.a. rising interest rates and tightening monetary policy). Whether or not the Fed will be able to quickly respond to changes in growth and whether or not we are headed for overheating will become more clear as we delve into the summer.

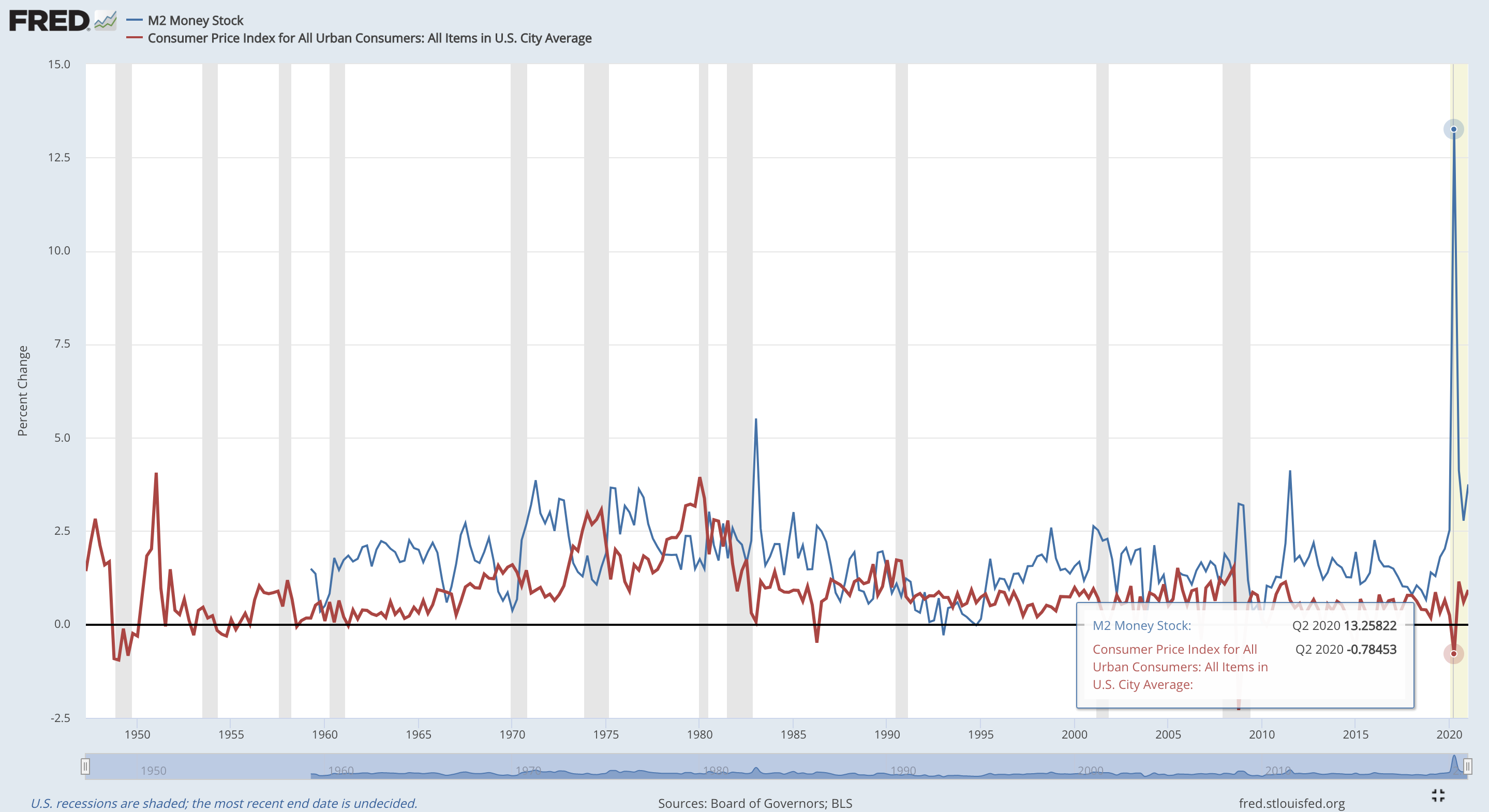

However, as it stands, inflation and the CPI still haven’t really kept up with the M2 increase we saw last summer.

Percent Change in M2 Money Stock from the M2SL FRED series plotted with the Percent Change in Consumer Price Index for All Urban Consumers: All Items in U.S. City Average, both quarterly and seasonally adjusted

Where’s the money going then? Assets, savings, consumer uncertainty, and unemployment all play a large role in why we haven’t seen price inflation just yet. Price inflation will show up when the M2 boost we saw begins circulating in the economy, not just because we see a rise in M2.

Lastly — something I can’t stress enough — the 2.6% annual rise in CPI is just that, a yearly rise. From March to May of 2020, we saw deflation, as spending outside of the household came to a screeching halt with lockdowns and unemployment. This 2.6% rise isn’t just a result of “money printing,” but a result of spending regressing to normal levels. What matters are core inflation numbers, and how CPI changes from here forward.

What’s next?

While markets tend to act immediately and with a lot of fear and volatility, it’s crucial to remember that the proposal is not set in stone, and will have to be passed by congress before being put to action, although with both the house and senate in a Democratic majority, it’s likely that there won’t be too much friction. Nonetheless, President Biden’s overall strategy paints a picture of an economic future where increases in fiscal spending seem inevitable.

Going forward, we’re likely to see an increase in the value and volume of individuals investing in assets typically seen as hedges against inflation, for at least the short-run. This includes precious metals and cryptocurrencies, as well as some commodities, to name a few.

Being mindful of what the Federal Reserve is doing will be of utmost importance, as a recent Fed minutes mentioned some talk of tapering, and a quick moving Fed has implications for interest rate rises and bond purchasing that can affect long-term assets like the purchase of homes, as well as assets seen as inflation hedges, mentioned above.

With so much future uncertainty and speculation it can be easy to get caught in a market-fearing mindset. My advice to you is easier said than done; don’t be startled, be cautious and informed.

And if inflation does run rampant, at least we’ll all be millionaires.

When I first visited Italy in 1999 I immediately went to a bank and converted my dollars into Lira so I could be a millionaire for the first time. That was about 630 US Dollars.

The energy and financial sectors need to cool off. People are getting tired of the bidding wars in the housing market too (at least I hope so). Time to build concrete houses like they do in the Caribbean, yo.