On the Fed's "Discontinuation" of the M2 Money Stock Data Series

Happy Monday!

I have taken a bit of a break from writing, due to final exams and traveling, but wanted to hop on and talk a bit about the Fed’s discontinuation of the M2 Money Stock data series and its replacement with the MS2L series, as I have seen an abundance of misinformation circling the web in both media and social networks.

The claim that the Fed has discontinued the reporting of the M2 money supply is not true; the Fed has not stopped reporting the money supply, but instead changed the frequency at which it is reported. I do not think much of this discourse was purposefully malicious, but mis-informed as the indicators and data series provided on FRED can be difficult to navigate and understand to non-economists.

Previously, the M2 data series was updated on a weekly basis, ending on Mondays. The M2 successor, M2SL, will be updated instead on a monthly basis. Regardless, this does not change whether or not we will be able to monitor changes in the monetary base, only the frequency at which it is made available.

What is the M2 Money Stock?

The money supply in the United States is broken down into various measures and monetary aggregate classifications, such as M0, M1, M2, and M3. The money supply can be broadly defined as the amount of money (or currency and other liquid instruments) that is in circulation or exists in a country’s economy. In order to better understand how these M’s operate and the implications they have, one can think of them as instruments representative of various types of money, with the money supply reflecting the different kinds of liquidity or spend-ability that each type of money represents.

The data series in question, M2, is a crucial indicator in most inflationary forecasting models, and thus its frequent reporting plays an important role in various economic models — likely the reason that its discontinuation stirred up so much attention.

Differences Between the M2 Data Series and the M2SL Data Series

As I mentioned above, the M2 data series reported the money base on a weekly basis, whereas the M2SL will report on a monthly basis. The switch was actually made on February 23, 2021, however, I have seen quite a majority of buzz around it over the past few weeks.

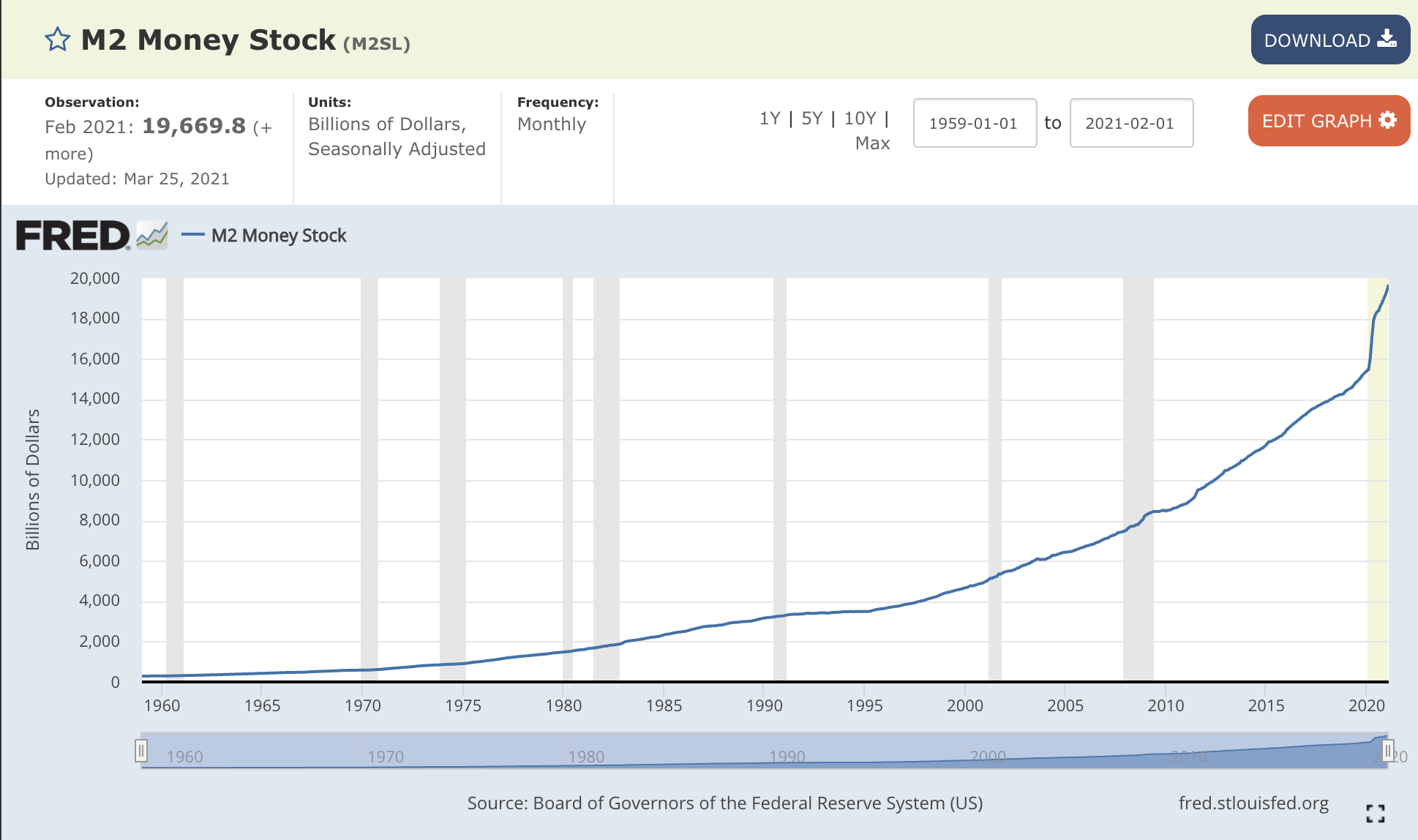

In a previous post, I briefly touched on the switch from M2 to M2SL, but have added the graphs for both data series below for an easy comparison. The following two charts look nearly identical, with the M2SL appearing to smooth weekly volatility to a minor extent:

Both data series are seasonally adjusted and accurately show the dramatic increase in the money base beginning after 2010. The series still correlates with rising inflation expectations, and while this could be stretched to argue that perhaps the Fed isn’t being as transparent, it is no cause for alarm and certainly not the Fed “shutting down its money supply data,” as some articles have claimed.

Why the switch?

Fed Chairman Jerome Powell has made it clear that he sees no issue with the rising monetary base and the potential for inflation to kick in this summer, as the economy recovers from the impact of the COVID-19 pandemic.

“Inflation is not a problem for this time as near as I can figure. Right now, M2 [money supply] does not really have important implications. It is something we have to unlearn.”

Jerome Powell, Chairman of the Federal Reserve

The Fed’s decision to switch to a regime of average inflation targeting from their previous 2% target is a whole other story I plan on addressing in a separate Substack post, but it is relevant to mention here, as M2 data plays a crucial role in the creation of inflationary indicators.

In addition, while the weekly average seasonally adjusted data is being replaced by the M2SL and will no longer be available, weekly non-seasonally adjusted M2 data will still remain available as the WM2NS, although it will only be updated on a monthly basis.

As Steve Hanke mentioned, the change in frequency of publication is likely due to the shifting of views held by the Fed, specifically regarding the role that the monetary base plays in predicting inflation. Perhaps the underlying motive was a decrease in transparency, but nonetheless, data will remain available.

Looking at the graphs for a smaller time range, the “smoothing” of the M2SL graph is a result no longer reporting weekly and instead averaging volatility. Both still wind up at level over 19,000, suggesting that the accuracy of this series remains in tact.

The cosmetic implications of this aside point to the potential for more complications in using this data for applications and models, as the number of observable points decreases with the decreased frequency of reporting. Thus, it would be harder to correlate weekly volatilities with various other variables.

Thinking Rationally

While there have been changes in the reporting of M2, I hope this serves as a reminder to not believe everything you read. I agree with Hanke’s consensus that the Fed doesn’t think this data is important and that their preference would likely be to publish as little of it as possible, however, I don’t think a switch from weekly to monthly data is too much of a cry for concern.

Be careful of reports that make bold claims about the suppression of data by the Fed and the role this plays in inflation narratives. While I’d like to attribute the problems of the world to bad Fed policy, that is frequently not the case. Again, I do not think much of the misinformation regarding M2 was spread maliciously, but in certain instances (such as the article linked above) it does seem that the changes are being used to push certain narratives. The M1 data series has also shifted from weekly to monthly, however, there hasn’t been much fluff about that since M2 is more relevant to inflation forecasting.

Overall, this isn’t meant to say anything about inflation, or my own expectations or targets of what we will see this summer, or whether the Fed’s decision is right or wrong. I just wanted to curb misinformation and bring some clarity to the switch from the M2 series to the M2SL series. My consensus is that the Fed is less concerned with the growth of the monetary base, as Powell has mentioned several times, and that this change is mainly aimed at reducing the weekly volatility we previously saw reported.

Talks of unlearning things? The amount of money in circulation will always be relevant to a central bank, whose levers at the end of the day basically just move the machinery of fiat money. I work with data science, and it's almost unfathomable to me that we'd want to decrease the fidelity of such a basic metric.

The biggest error in the history of the world is that banks loan out deposits (that they are intermediaries). Not so. Deposits are the result of lending/investing, not the other way around. All bank-held savings are un-used and un-spent, lost to both consumption and investment, indeed to any type of payment or expenditure. That is the sole source of Alvin Hansen's secular strangulation, not robotics, not globalization, not demographics, not monopolization.

The demarcation between 1961 and 1981 was due to the end of the "monetization of time deposits". Everything that has happened was predicted in “Should Commercial Banks Accept Savings Deposits?” Conference on Savings and Residential Financing 1961 Proceedings, United States Savings and loan league, Chicago, 1961, 42, 43